Since the advent of Covid-19: buying and selling habits have changed. For a while, everything stopped quickly. So consumers began shopping online for almost everything, forcing producers to prepare for those purchases. However, what we see now is a continuous growth in the purchase of goods, especially those that need to be shipped internationally. But is our biggest buying thirst hurting the supply chain?

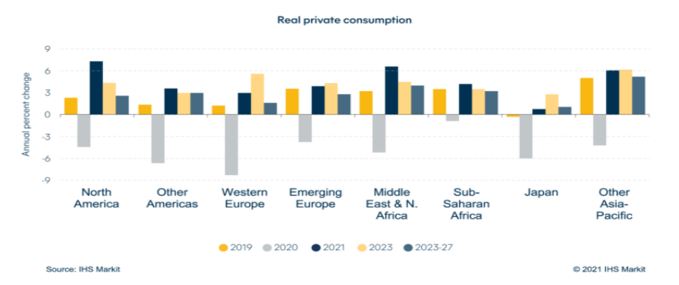

Take the US, for example, they recorded more than 20% growth in April (vs April 2020 or 6.8% vs April 2019) in consumer spending, which is a big increase in sales. Great for recovering much-depleted cash from the pandemic, but it also meant record inventory and pressure on an already tense ocean container market.

So while the ability to ship with confidence remains low and unprecedented, the demand for containers to pack and prepare cargo for any voyage you might take, reaches an all-time high.

Most of this growth is concentrated in US demand. North American imports increased 33.6% in the first four months of the year, reaching 10.9 million TEU. In addition, almost 70% of total US imports are manufactured in Asia, which grew 45.0% compared to last year.

It is also worth opening a parenthesis and mentioning how this has strongly affected Brazil. The automotive sector is the most impacted, because it is part of the global chain. The risk of interruptions at automakers remains permanent. We live in times of great stress in the logistic channels. In Jan/21, the port of Santos set a historical record for handling, both in general and in containers, with the mark of 338,500 TEUS, an increase of 10.5% compared to Jan/20. Brasil. O setor automobilístico é o mais impactado, porque está dentro da cadeia global. O risco das interrupções nas montadoras continua permanente. Vivemos tempos de muito estresse nos canais logísticos. Haja visto que, em Jan/21, o porto de Santos bateu recorde histórico de movimentação, tanto geral quanto de contêineres, com a marca de 338,5 mil TEUS, alta, de 10,5% em relação a Jan/20.

Mas voltemos a referência aos EUA e à Ásia, que são dois países problemáticos agora e ambos lutam com as operações de cais de baixo desempenho, especialmente em Oakland e Yantian, com um tempo de espera para atracação em torno de 14 dias. Em abril, apenas 39% das embarcações estavam no prazo.

For operators, it's all a big global balancing act. Strong demand in one place requires an injection of capacity and supply. But, this comes at the cost of getting it from somewhere else. At the moment, demand is growing everywhere, and due to container imbalances mainly between the troubled two and the container production at stake, we've all become well versed in the consequences:

In more alarming data: in April, 2.1 million TEUs (8.6% of the nominal container fleet) were missing, or more accurately, they were tied to ship delays. This is literally the equivalent of taking the entire global fleet of container ships capable of carrying more than 18,000 TEUs from the seas. For a deeper context, last week there were around 300 ships waiting to dock at Yantian port.

15% to 20% of the global container fleet is 'unavailable'!!

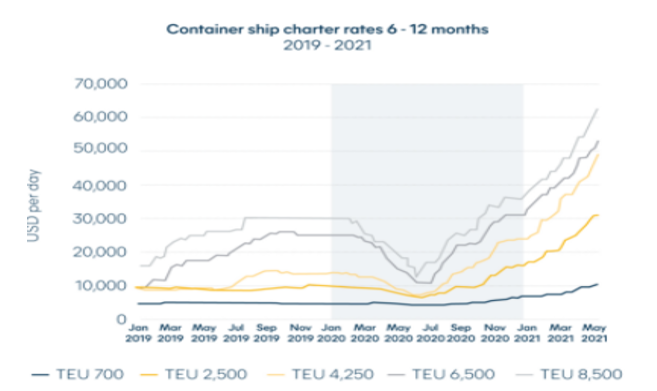

Until 2023, when new container ships go to sea, capacity growth will hardly meet demand. Costs are unlikely to improve either. To get an idea of the operating costs of chartering today, there is a contract signed for the next few months for $148,000 per day!

It's really not looking good for the upcoming peak season, although some good news has surfaced in the last few days; The Suez Canal Authority (SCA) and the Ever Given shipowner reached an agreement in principle on the pending indemnity claim. In addition, Yantian port is back to full operational operation after clearing 21 consecutive days with no new Covid-19 cases.

The general recommendation is to consider:

For warehousing and transport services with third parties and/or international transport management, contact us at: + 55 11 972233612

from: Fabrícia Anjos

Source: Hillebrand

{kind=link}